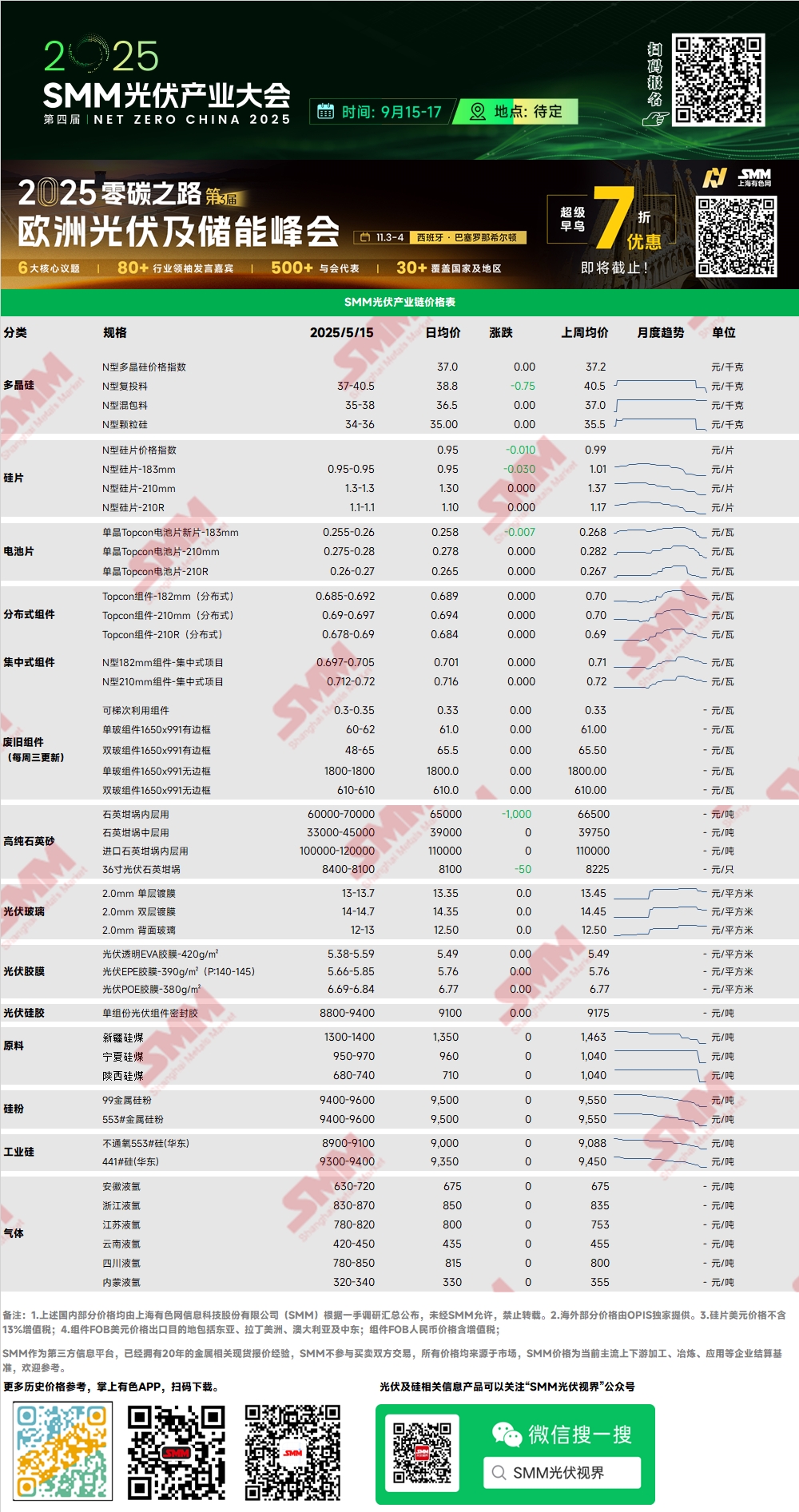

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon in the market ranged from 37 to 42 yuan/kg, with the N-type polysilicon price index at 37 yuan/kg. In the early part of the week, major polysilicon producers stood firm on quotes, but prices pulled back again later when quoting to crystal pulling plants. Currently, the expected transaction price for mixed polysilicon from major producers is around 36 yuan/kg. An industry meeting was held again on Wednesday to discuss matters related to production cuts. Currently, polysilicon production in May is expected to be around 94,000 mt. Prices in the downstream market have been falling more frequently recently, and there is still upward pressure on prices in the future market.

Wafer: This week, the price of domestic N-type 18Xmm wafers was 0.95 yuan/piece, N-type 210R wafers were priced at 1.1 yuan/piece, and N-type 210mm wafers were priced at 1.3 yuan/piece. The overall market sentiment is poor, with downstream price-driving being common, and wafer prices have fallen again. Taking the 183 type as an example, individual large-volume low-price quotations have dropped as low as 0.93 yuan/piece. Some wafer enterprises further cut production in the early part of May, and currently, domestic wafer production is expected to exceed 55GW, with global production exceeding 58GW.

Cell: For P-type cells, the mainstream quotation for 182P has slipped to the range of 0.29 yuan/W, with the overall demand scale continuing to shrink. For N-type cells, the mainstream quotation for 183N is 0.26 yuan/W, with quotations ranging from 0.255 to 0.26 yuan/W, 210RN at 0.26 to 0.27 yuan/W, and 210N at 0.28 to 0.285 yuan/W. Among these, the prices of 210RN and 210N are relatively stable. 210RN is currently in a tight balance, with limited external supply and a temporary halt in the downward price trend. The price of 183N fell rapidly this week, mainly due to weak market demand. Module plants, holding higher bargaining power, continuously drove down prices, and solar cell plants, facing inventory pressure, shipped within this price range. Currently, specialized and integrated plants are considering further production cuts to alleviate inventory pressure in late May. It is expected that in the short term, cell prices will continue to oscillate downward after entering the current bottom platform period due to supply-demand imbalance and the impact of wafer prices.

Module: This week, the prices of PV modules continued to decline. The mainstream transaction price for N-type 182mm modules in centralized projects ranged from 0.697 to 0.705 yuan/W, with the average price decreasing by 0.004 yuan/W. The mainstream transaction price for N-type 210mm modules ranged from 0.712 to 0.72 yuan/W, with the average price decreasing by 0.004 yuan/W. The price of distributed N-type 182 modules was around 0.685 to 0.692 yuan/W, with the average price decreasing by 0.01 yuan/W compared to last Friday. The price of distributed N-type 210 modules was 0.69 to 0.697 yuan/W, with the average price decreasing by 0.01 yuan/W compared to last Friday. The price of distributed N-type 210R modules was 0.678 to 0.69 yuan/W, with the average price decreasing by 0.008 yuan/W compared to last Friday. This week, the inversion phenomenon between distributed and centralized modules has eased somewhat, and there is a trend for module prices to stabilize at the bottom in the short term. Currently, local governments have successively introduced policies to implement Document No. 136, and terminal clients are still awaiting bidding notifications to calculate their investment yields. This week, the Photovoltaic Industry Association provided benchmark prices for current modules as guidance. It is understood that violations of relevant regulations may result in being blacklisted. SMM analyzed that this measure will contribute to the short-term stabilization of module prices.

Terminal: From May 5, 2025, to May 11, 2025, SMM recorded a total of 27 domestic enterprises winning bids for PV module projects during the week. The winning bid prices for PV modules were concentrated in the range of 0.66-0.87 yuan/W, with a weighted average price of 0.76 yuan/W for the week, an increase of 0.01 yuan/W compared to the previous week. The total procurement capacity of winning bids was 263.77 MW, an increase of 220.44 MW compared to the previous week.

Film: The mainstream price range for EVA film is 13,000-13,200 yuan/mt, while the price range for EPE film is 14,500-15,000 yuan/mt. On the cost side, the price of PV-grade EVA has fallen, weakening cost support. On the demand side, module prices have declined, leading to a drop in demand. Under the dual pressure of cost and demand, film prices have decreased.

EVA: This week, the price of PV-grade EVA ranged from 10,500-10,700 yuan/mt, with the transaction center continuing to decline. The prices of foaming-grade and cable-grade EVA have also seen significant decreases. On the demand side, film prices have fallen, compressing the price spread and forcing the raw material side to offer discounts. The overall market sentiment is one of wait-and-see, and it is expected that EVA prices will continue to decline in the later period.

POE: The domestic delivery-to-factory price of POE remains stable at 12,000-14,000 yuan/mt. Despite some petrochemical enterprises still being in maintenance cycles, under the dual impact of weak demand and the gradual release of new capacity, the market price of PV-grade POE is expected to fluctuate downward.

PV Glass: This week, the benchmark prices quoted by some PV glass enterprises have remained stable. As of now, the mainstream quotation for 2.0mm single-layer coated PV glass in China is 13.5 yuan/m², with some enterprises reducing their quotations to 13 yuan/m². The mainstream quotation for 3.2mm single-layer coated PV glass is 22.0 yuan/m², and the mainstream quotation for 2.0mm back-glass is 12.0 yuan/m². This week, the high prices in the domestic PV glass market have slightly loosened. As of now, the quotation for 2.0mm single-layer coated PV glass is 13-13.7 yuan/m². Due to the recent sluggish purchasing sentiment of module enterprises, glass enterprises still maintain an attitude of offering discounts. Despite still having profits, glass market quotations began to decline this week. However, the sentiment of module enterprises has not yet been stimulated. Against the backdrop of continuously falling module prices, module enterprises have maintained a low-volume, just-in-time purchasing model. It is expected that the next purchasing period will be at the end of next week, with a target purchasing price of 13 yuan/m². Therefore, the recent glass market price negotiations have reached a stalemate. On the supply side, there was no new capacity release this week. However, some products from kilns that started production earlier began to enter the market, and the overall market supply is expected to continue increasing.

High-purity quartz sand: This week, the price quotes for some domestic high-purity quartz sand products still maintained a downward expectation. The current market quotes are as follows: Inner layer sand is priced at 60,000-70,000 yuan/mt, with a 3,000 yuan/mt reduction from the high price. Middle layer sand is priced at 33,000-45,000 yuan/mt, with prices remaining stable. Outer layer sand is priced at 18,000-24,000 yuan/mt, with a 1,000 yuan/mt reduction from the high price. Domestic wafers continued to face downward price pressure this week. Against the backdrop of weakening wafer production schedules and prices, wafer manufacturers have a strong intention to suppress raw material purchases. Consequently, the prices of domestic sand began to decline slightly this week. Meanwhile, the recent cancellation of some tariffs in the trade war has alleviated the shortage sentiment for imported sand. Recently, some crucible enterprises have started negotiating prices with imported sand suppliers. Affected by the weakening demand, imported sand prices are also expected to decline, with long-term contract prices possibly falling below 90,000 yuan/mt and spot order prices possibly dropping below 95,000 yuan/mt.

》View the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)